Nonparametric statistics

This is the practical lab tutorial for nonparametric

statistics. But we shall start with a little theory that will be

crucial for understanding the underlying concepts.

Distributions

In statistics we often come across questions like

``Is a given data from such-n-such distribution?''

Before we can answer this question we need to know what is meant

by a distribution. We shall talk about this first.

In statistics, we work with random

variables. Chance controls their values.

The distribution of a random variable is the rule by which

chance governs the values.

If you know the distribution then you know the

chance of this random variable taking value in any given range.

This rule may be expressed in various ways. One popular way is

via the Cumulative Distribution Function (CDF), that we

illustrate now. If a random variable (X) has distribution with CDF

F(x) then for any given number a the chance that

X will be ≤ a is F(a).

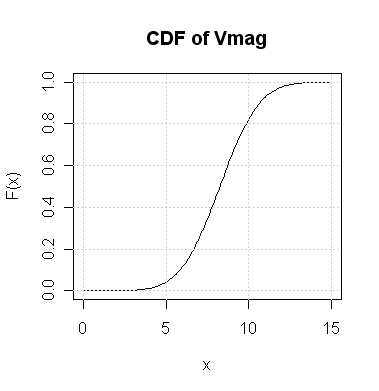

| Example:

Suppose that I choose a random star from the Hipparcos data

set. If I tell you that its Vmag is a random variable

with the following CDF then what is the chance that it takes values

≤ 10? Also find out the value x such that

the chance of Vmag being ≤ x is 0.4.

For the first question the required probability is F(10)

which, according to the

graph, is slightly above 0.8.

In the second part we need F(x) = 0.4. From the graph it

seems to be about 7.5.

Just to make sure that these are indeed meaningful, let us load

the Hipparcos data set and check:

hip = read.table("HIP.dat", header = TRUE, fill = TRUE)

attach(hip)

n = length(Vmag) #total number of cases

count = sum(Vmag <= 10) #how many <= 10

count/n #should be slightly above 0.8

This checks the answer of the first problem. For the second

count = sum(Vmag <= 7.5) #how many <= 7.5

count/n #should be around 0.4

|

So you see how powerful a CDF is: in a sense it stores as much

information as the entire Vmag data. It is a

common practice in statistics to regard the distribution as the

ultimate truth behind the data. We want to infer about the

underlying distribution based on the data.

R has many standard distributions already built into it. This

basically means that R has functions to compute their CDFs.

These functions all start with the letter p.

| Example:

A random variable has standard Gaussian distribution. We know

that R computes its CDF using the function pnorm. How to

find the probability that the random variable takes values

≤ 1?

The answer may be found as follows:

pnorm(1)

|

For every p-function there is a

q-function that is basically its inverse.

| Example:

A random variable has standard Gaussian distribution. Find

x such that the random variable is ≤ x with

chance 0.3.

Now we shall use the function qnorm:

qnorm(0.3)

|

OK, now that we are through our litttle theory session, we are

ready for the nonparametric lab.

One sample nonparametric tests

Sign-test

In a sense this is the simplest possible of all tests. Here

we shall consider the data set LMC.dat that stores the measured

distances to the Large Magellanic Cloud.

LMC = read.table("LMC.dat",head=T)

data = LMC[,2] #These are the measurments

data

We want to test if the

measurements exceed 18.41 on an average. Now, this does

not

mean whether the average of the data exceeds 18.41, which is trivial

to find out. The question here is actually about the underlying

distribution. We want to know if the median of the underlying

distribution exceeds 18.41, which is a less trivial question,

since we are not given that distribution.

We shall use the sign test to see if the median is 18.41 or larger.

First it finds how many of the

observations are above this value:

abv = sum(data>18.41)

abv

Clearly, if this number is large, then we should think that the

median (of the underlying distribution) exceeds 18.41. The

question is how large is ``large

enough''? For this we consult the binomial distribution to get

the p-value. The rationale behind this should come from

the theory class.

n = nrow(LMC)

pValue = 1-pbinom(abv-1,n,0.5)

pValue

We shall learn more about p-values in a later

tutorial. For now, we shall use the following rule of thumb:

If this p-value is below 0.05, say, we shall conclude that

the median is indeed larger than 18.41.

Wilcoxon's Signed Rank Test

As you should already know from the theoretical class, there is a

test called Wilcoxon's Signed Rank test that is better (if a little

more complicated) than the sign test. R provides the function

wilcox.test for this purpose. We shall work with the

Hipparcos data set this time, which we have already loaded.

We want to see if the median of the distribution of the

pmRA variable is 0 or not.

wilcox.test(pmRA, mu=0)

Since the p-value is pretty large (above 0.05, say) we

shal conclude that the median is indeed equal to 0. R itself

has come to the same conclusion.

Incidentally, there is a little caveat. For Wilcoxon's Rank Sum Test

to be applicable we need the underlying distribution to be

symmetric around the median. To get an idea about this we should

draw the histogram.

hist(pmRA)

Well, it looks pretty symmetric (around a centre line).

But would you apply Wilcoxon's

Rank Sum Test to the variable DE?

hist(DE)

No, this is not at all symmetric!

Kolmogorov-Smirnov test

The theory class has talked about a non-parametric test called

Kolmogorov-Smirnov test. We shall cover it in a later tutorial.

k-nearest neighbours

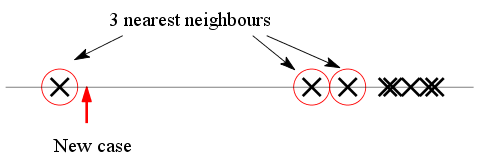

Imagine that you are given a data set of average parent heights

and their adult sons' heights, like this (ignore the colour for

the time being):

Parent Son

5.5 5.9

5.4 5.3

5.7 5.9

5.1 5.3

6.0 5.8

5.5 5.2

6.1 6.0

A prosepective

couple comes to you, reports that their average height is 5.3

feet, and wants you to predict (based on this data set) the

height their son would attain

at adulthood. How should you proceed?

A pretty simple method is this: look at the cases in your data

set with average parents' height near 5.3. Say, we consider the 3

nearest cases. These are shown in red in the above data

set. Well, there are 4 cases, and not 3. This is because there

is a tie (three cases 5.1, 5.5, 5.5 that are at same

distance from 5.3).

Now just report the average of the sons' height for these cases.

Well, that is all there is to it in 3-NN regression (NN = Nearest

Neightbour)! Let us

implement this in R. First the data set

parent = c(5.5, 5.4, 5.7, 5.1, 6.0, 5.5, 6.1)

son = c(5.9, 5.3, 5.9, 5.3, 5.8, 5.2, 6.0)

Now the new case:

newParent = 5.3

Find the ditances of the parents' heights from this new height:

d = abs(parent- newParent)

Rank these:

rnk = rank(d,tie="min")

rnk

Notice the tie="min" option. This allows

the three joint seconds to be each given rank 2.

We are not using order here (as it does not handle ties

gracefully). Now identify the 3 nearest cases (or more in case of

ties).

nn = (rnk<=3)

nn

Now it is just a matter of taking averages.

newSon = mean(son[nn])

newSon

It is instructive to write a function that performs the above

computation.

knnRegr = function(x,y,newX,k) {

d = abs(x-newX)

rnk = rank(d,tie="min")

mean(y[rnk<=k])

}

Now we can use it like

newSon = knnRegr(parent,son,newParent,3)

| Exercise:

You shall apply the function that we have just written to the

Hipparcos data set.

plot(RA,pmRA)

We want to explore the relation between RA and

pmRA using the k-nearest neighbour

method.

Our aim is to predict the value pmRA based on a

new value of RA:

newRA = 90.

Use the knnRegr function to do this with k=13.

|

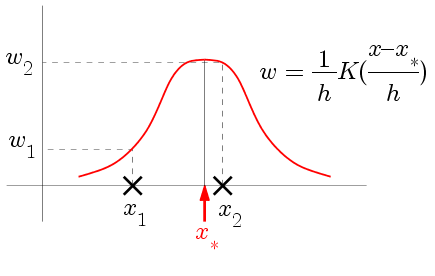

Nadaraya-Watson regression

While the k-nearest neighbour method is simple and

reasonable it is nevertheless open to one objection that we illustrate

now. Suppose that we show the x-values along a number line

using crosses as below. The new x-value is shown

with an arrow. The 3 nearest neighbours are circled.

|

| Are the 3 NN equally relevant? |

The k-NN method now requires us to simply average the

y-values of the circled cases. But since two of the points

are rather far away from the arrow, shouldn't a weighted

average be a better method, where remote points get low

weights?

This is precisely the idea behind the Nadaraya-Watson

regression. Here we average over all the cases (not just

nearest neighbours) but cases farther away get less weight. The

weights are decided by a kernel function (typically a

function peaked at zero, and tapering off symmetrically on both

sides).

|

| How the kernel determines the weights |

Now we may simply take the weighted average. We shall apply it to

our parent-son example first.

parent = c(5.5, 5.4, 5.7, 5.1, 6.0, 5.5, 6.1)

son = c(5.9, 5.3, 5.9, 5.3, 5.8, 5.2, 6.0)

newParent = 5.3

kernel = dnorm #this is the N(0,1) density

Now let us find the weights (for a bin width (h) = 0.5, say):

h = 0.5

wt = kernel((parent- newParent)/h)/h

Finally the weighted average:

newSon = weighted.mean(son,w = wt)

| Exercise:

Write a function called, say, nw, like this

nw = function(x,y,newX,kernel,h) {

#write commands here

}

[Hint: Basically collect the lines that we used just now.]

Now use it to predict the value of pmRA when

RA is 90 (use h=0.2):

newRA = 90

newpmRA = nw(RA,pmRA,newRA,dnorm,0.2)

|

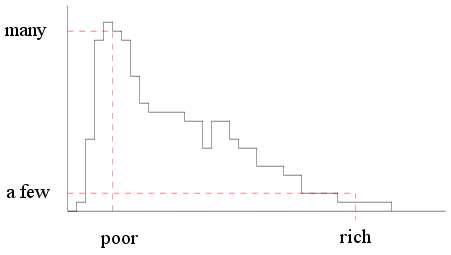

Two-sample nonparametric tests

Here we shall be taking about the shape of distributions. Let us

first make sure of this concept. Suppose that I make a list of

all the people in a capitalist country

and make a histogram of their incomes.

I should get a histogram like this

|

| Income histogram of a capitalist

country |

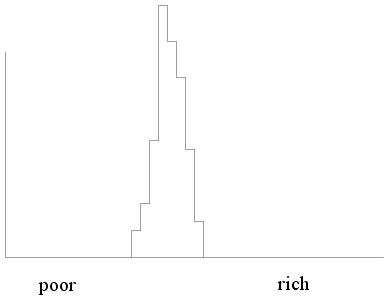

But if the same thing is done for a socialist country we shall

see something like this (where almost everybody is in the middle

income group).

|

| Income histogram of a socialist

country |

Clearly, the shapes of the histograms differ for the two

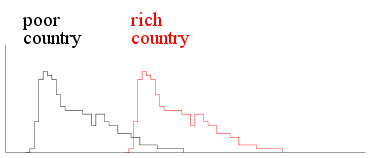

populations. We must be careful about the term ``shape'' here. For

example, the following two histograms are for two capitalist

countries, one rich the other poor.

|

| Income histograms two capitalist

countries |

Here the histograms have the same shape but differ in

location. You can get one from the other by applying a

shift in the location.

This is a very common phenomon in statistics. If we have two

populations with comparable structure they often have similar

shapes, and differ in just a location shift. In such a situation

we are interested in knowing about the amount of shift. if the

amount of shift is zero, then the two populations behave

identically.

Wilcoxon's rank sum test is one method to learn about the amount

of shift based on samples from the two populations.

We shall start with the example done in the theory class, where

we had two samples

x = c(37,49,55,57)

y = c(23,31,46)

m = length(x)

n = length(y)

We are told that both the samples come from populations with the

same shape, though one may be a shifted version of the

other.

Our aim is to check if indeed there is any shift or not.

We shall consider the pooled data (i.e., all the 7 numbers

taken together) and rank them

pool = c(x,y)

pool

r = rank(pool)

r

The first m=4 of these ranks are for the first

sample. Let us

sum them:

H = sum(r[1:m])

H

If the the two distributions are really identical (i.e.,

if there is no shift) then we should have (according to the

theory class) H close to the value

m*(m+n+1)/2 #Remember: * means multiplication

Can the H that we computed from our data be considered

``close enough" to this value? We shall let us R determine that

for us.

wilcox.test(x,y)

So R clearly tells us that there is a shift in location. The

output also mentions a W and a

p-value.

tutorial. But W is essentially what we had called

H. Well, H was 21, while W is 11. This

is because R has the habit of subtracting

from H and calling it W. Indeed for our data set

which perfectly accounts for the difference between our H

and R's W.

You may recall from the theory class that H is called

Wilcoxon's rank sum statistic, while W is the Mann-Whitney

statistic (denoted by U in class).

Now that R has told us that there is a shift, we should demand to

estimate the amount of shift.

wilcox.test(x,y,conf.int=T)

The output gives two different forms of estimates. It

gives a single value (a point estimate) which is 16.

Before it gives a 95% confidence interval: -9 to

34.

This

basically means that

we can say with 95% confidence that

the true value of the shift is between -9 and 34.

We shall talk more about confidence intervals later. For now let

us see how R got the poit estimate 16. It used the so-called

Hodges-Lehman formula, that we have seen in the theoretical

class. To see how this method works we shall first form the following

"differecne table"

| 23 31 46

------------

37| 14 6 -9

49| 26 18 3

55| 32 24 9

57| 34 26 11

Here the rows are headed by the first sample, and coumns by the

second sa,mple. Each entry is obtained by subtracting the column

heading from

the row heading (e.g., -9 = 37-46). This table, by the

way, can be created very easily with the function outer.

outer(x,y,"-")

|

|  |  |

|

The outer function is a very useful (and somewhat

tricky!) tool in R. It takes two vectors x, and y,

say, and some function f(x,y). Then it computes a matrix

where the (i,j)-th entry is

| |

| |  |

|

Now we take the median of all the entries in the table:

median(outer(x,y,"-"))

This gives us the Hodges-Lehman estimate of the location shift.